By Sung Won Sohn

The author is professor of finance and economics at Loyola Marymount University and president of SS Economics. He was executive vice president at Wells Fargo Banks and senior economist on the President’s Council of Economic Advisors in the White House.

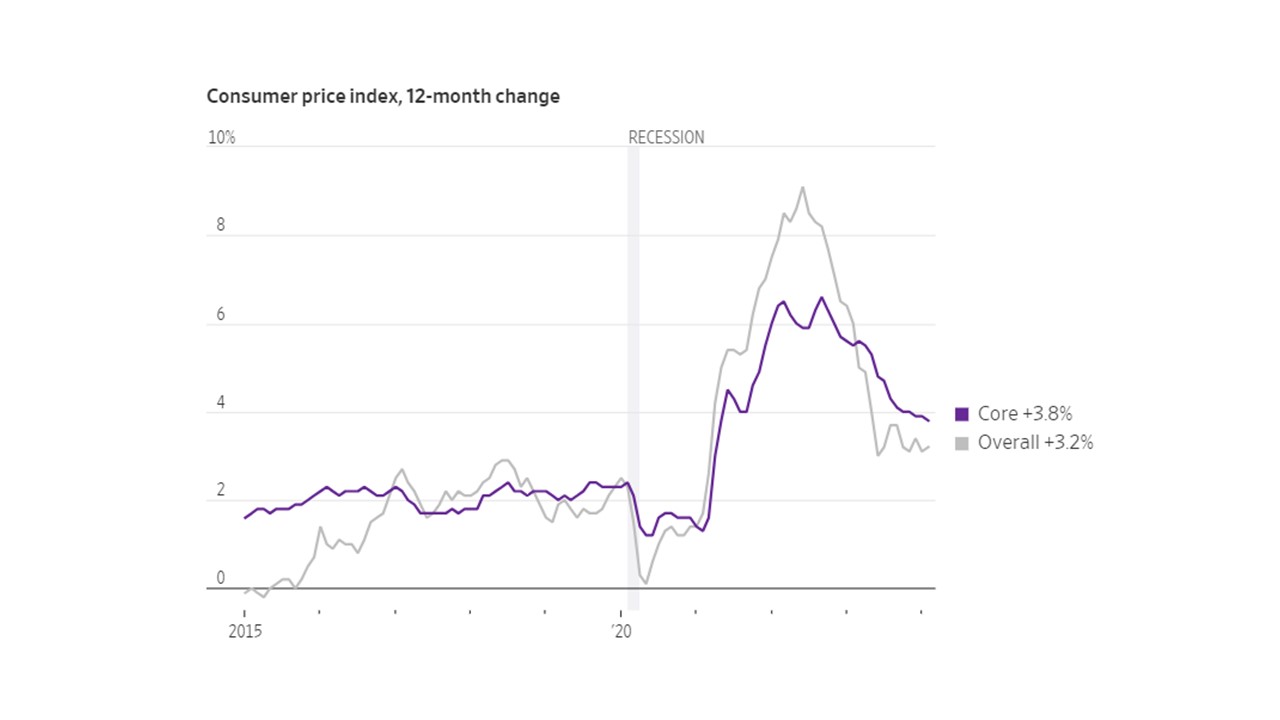

Inflation is like a bobsled track. It slopes down with many twists and turns.

In February, the CPI accelerated to 3.2 percent from a year ago vs. 3.1 percent in January. The rising price of gasoline along with shelter were the primary culprits accounting for 60 percent of the increase in the price index.

The uptick in the inflation rate supports the Federal Reserve’s “go-slow” approach to cutting the interest rate. What is important is that the overall inflation trend is downward from the peak of 9.1 percent in June 2022.

Given the stubborn price increases, the Federal Reserve is in no hurry to cut the interest rate. The “last mile” problem for the central bank is the inflation in service prices, which is partly attributed to the tight labor market in sectors such as healthcare, leisure, hospitality, and construction.

This has led to increasing costs for services ranging from dining out to personal care and home repair. This type of inflation, often termed “cost-push inflation”, may not react straightforwardly to changes in interest rates. Factors such as substantial labor settlements, hikes in minimum wages, and slow productivity growth are contributing to this inflationary pressure.

One good news for Chairman Powell and his colleagues is that “the super-core”, which is service price excluding shelter, slowed to 0.5 percent from 0.7 percent in January; this index is closely watched by the central bank. As shelter costs with their 34 percent weight in the CPI are expected to fall later this year, the downward trend in inflation should continue.

In summary, while there are clear signs of inflation cooling down, leading to expectations of lower interest rates. The course of future monetary policy will need to balance these mixed signals, considering both the encouraging trends in goods prices and the persistent challenges in the services sector. The Federal Reserve needs additional positive inflation data to feel comfortable about cutting the interest rate.

{kind=link}